New Construction vs. Resale Homes: 2025 Austin Area Housing Market Insights

Published | Posted by Dan Price

New Construction vs. Resale Homes: A Data-Driven Look at the Austin Area Housing Market in 2025

The Austin area housing market in 2025 presents a dynamic landscape where new construction and resale homes vie for buyer interest. A comprehensive dataset from Team Price Real Estate, updated on April 17, 2025, offers a detailed comparison of these markets across 30 cities in the Austin region, including Austin, Buda, Pflugerville, and Del Valle. The dataset tracks active listings, pending sales, sold homes, activity index, and months of inventory. The activity index, calculated as pending sales divided by the sum of active and pending listings, shows the percentage of homes under contract, reflecting market momentum. Months of inventory indicates how long it would take to sell all active listings at the current sales rate. This article delves into these metrics to provide a clear view of the Austin area’s real estate trends.

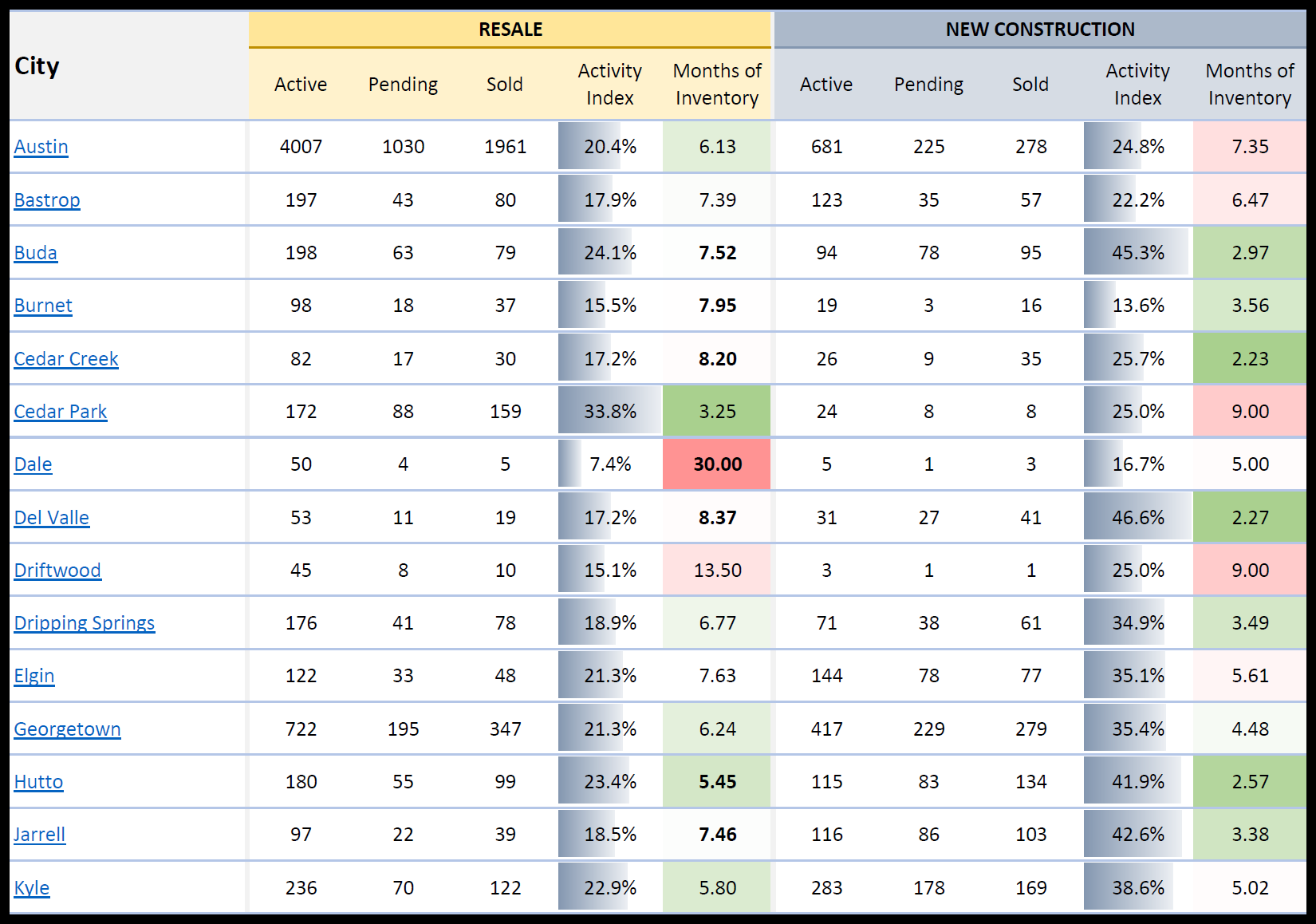

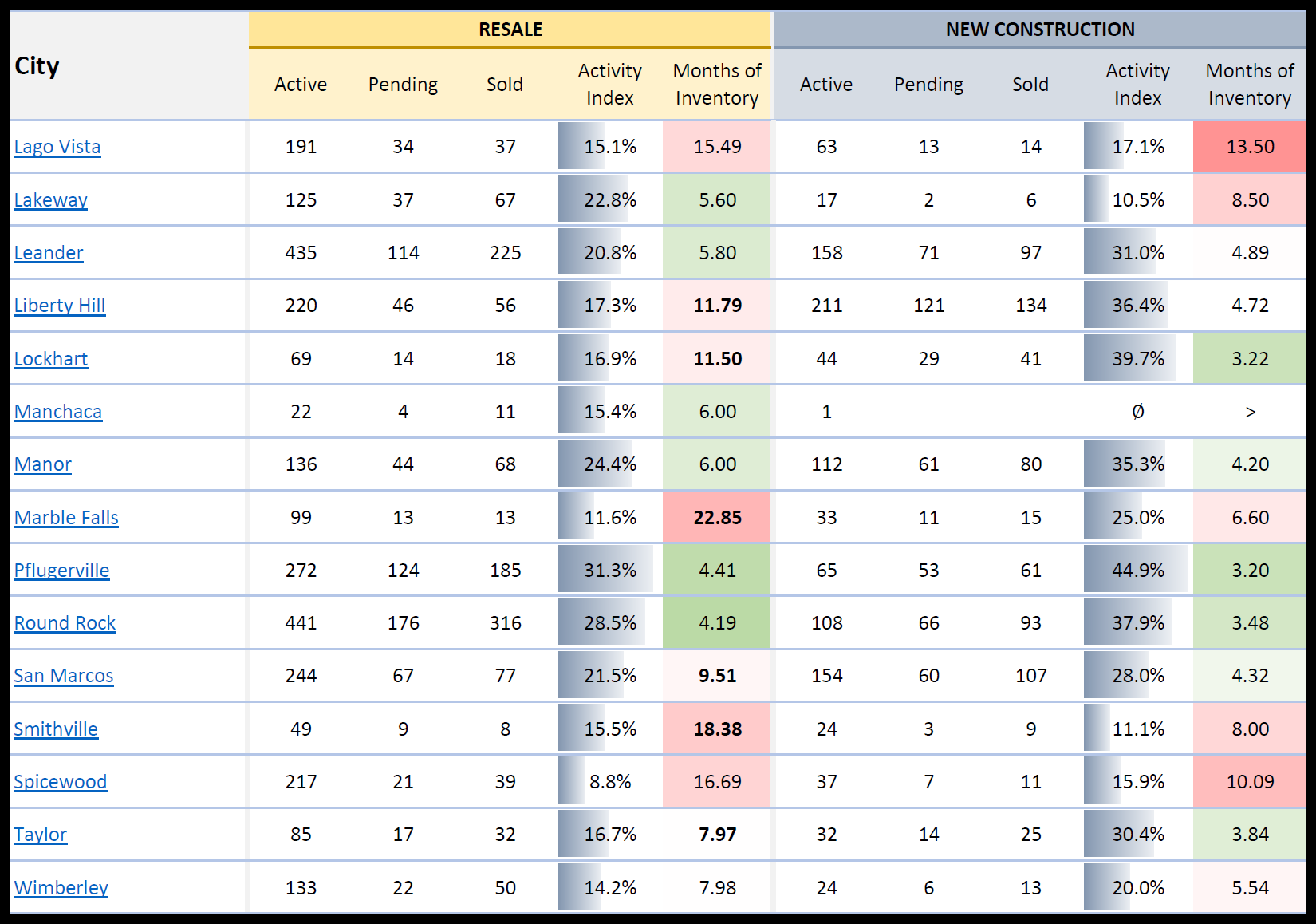

In Austin, the resale market is substantial, with 4,007 active listings, 1,030 pending sales, and 1,961 homes sold. The activity index is 20.4%, meaning roughly one in five available or pending homes is under contract. With 6.13 months of inventory, Austin’s resale market leans toward balance. New construction in Austin, by contrast, has 681 active listings, 225 pending sales, and 278 sold homes, yielding a higher activity index of 24.8% but a slightly elevated 7.35 months of inventory. This suggests new homes in Austin face a marginally slower sales pace than resales, despite stronger buyer engagement.

Buda’s new construction market shines brightly. With 94 active listings, 78 pending sales, and 95 sold homes, new homes in Buda achieve a 45.3% activity index, one of the highest in the dataset. The 2.97 months of inventory signals a strong seller’s market where homes move quickly. Buda’s resale market, with 198 active listings, 63 pending sales, and 79 sold homes, posts a respectable 24.1% activity index but a higher 7.52 months of inventory, indicating resale homes take longer to sell. This contrast highlights how new construction can dominate buyer interest in certain areas.

Pflugerville also showcases robust new construction activity. With 65 active listings, 53 pending sales, and 61 sold homes, new homes have a 44.9% activity index and a low 3.20 months of inventory, reflecting high demand. The resale market, with 272 active listings, 124 pending sales, and 185 sold homes, has a 31.3% activity index and 4.41 months of inventory. While healthy, the resale market lags behind new construction, suggesting buyers in Pflugerville may prioritize modern homes.

Del Valle exemplifies the appeal of new construction in smaller markets. With 31 active listings, 27 pending sales, and 41 sold homes, new homes in Del Valle boast a 46.6% activity index and just 2.27 months of inventory, indicating a hot market. Resale homes, with 53 active listings, 11 pending sales, and 19 sold homes, show a 17.2% activity index and 8.37 months of inventory, reflecting slower sales. Similarly, Hutto’s new construction market, with 115 active listings, 83 pending sales, and 134 sold homes, has a 41.9% activity index and 2.57 months of inventory, compared to a 23.4% activity index and 5.45 months for resales.

Georgetown, a significant market, shows balanced activity. New construction includes 417 active listings, 229 pending sales, and 279 sold homes, with a 35.4% activity index and 4.48 months of inventory. Resale homes, with 722 active listings, 195 pending sales, and 347 sold homes, have a 21.3% activity index and 6.24 months of inventory. This suggests new homes in Georgetown move faster, likely due to contemporary features appealing to buyers.

Smaller markets like Manchaca reveal challenges for new construction. With only one active listing and no pending or sold homes, the activity index is 0%, and inventory is undefined. Resale homes in Manchaca, with 22 active listings, 4 pending sales, and 11 sold homes, have a 15.4% activity index and 6.00 months of inventory, indicating modest activity. Marble Falls’ resale market, with 99 active listings, 13 pending sales, and 13 sold homes, has an 11.6% activity index and a high 22.85 months of inventory, signaling a sluggish market. New construction in Marble Falls, with 33 active listings, 11 pending sales, and 15 sold homes, performs better with a 25.0% activity index and 6.60 months of inventory.

Lago Vista and Spicewood reflect slower markets. Lago Vista’s new construction, with 63 active listings, 13 pending sales, and 14 sold homes, has a 17.1% activity index and 13.50 months of inventory. Resale homes, with 191 active listings, 34 pending sales, and 37 sold homes, show a 15.1% activity index and 15.49 months of inventory. Spicewood’s resale market, with 217 active listings, 21 pending sales, and 39 sold homes, has an 8.8% activity index and 16.69 months of inventory, while new construction, with 37 active listings, 7 pending sales, and 11 sold homes, has a 15.9% activity index and 10.09 months of inventory.

How This Data Helps Sellers Compete with New Construction

For sellers of resale homes in the Austin area, this data is a powerful tool to navigate competition from new construction, especially in cities where new homes dominate. In places like Buda, Del Valle, and Hutto, the new construction market appears “healthy” with high activity indices (45.3%, 46.6%, and 41.9%, respectively) and low months of inventory (2.97, 2.27, and 2.57 months). Meanwhile, resale markets in these cities show higher inventory (7.52, 8.37, and 5.45 months) and lower activity indices (24.1%, 17.2%, and 23.4%), suggesting resale homes face stiffer competition. Sellers can use this data creatively to stand out.

One out-of-the-box approach is to leverage the data to highlight unique neighborhood features. In Buda, where new construction inventory is low, resale sellers can emphasize established community amenities—like mature trees, local schools, or proximity to downtown—that new developments may lack. By marketing their home as a “move-in ready classic” with upgrades mimicking new builds (e.g., fresh paint or modern fixtures), sellers can appeal to buyers drawn to new construction’s polish but deterred by limited availability.

Another strategy is to use the activity index to time the market. In Del Valle, the 46.6% activity index for new construction versus 17.2% for resales suggests builders are capturing buyers. Resale sellers could analyze pending sales data to identify peak buyer activity periods and list their home when new construction pending sales dip, reducing competition. Hosting virtual tours with interactive neighborhood maps could further differentiate their property, showcasing lifestyle benefits over new homes’ generic appeal.

Sellers in high-inventory resale markets like Marble Falls (22.85 months) can use the data to pivot creatively. With new construction at a 25.0% activity index versus 11.6% for resales, sellers might collaborate with local businesses to offer buyer incentives, such as a year of free landscaping or gym memberships, to mimic the perks builders provide. Highlighting energy-efficient retrofits, like solar panels or smart thermostats, can also position a resale home as a sustainable alternative to new builds.

In Austin, where resale inventory (6.13 months) is slightly lower than new construction (7.35 months), sellers can capitalize on the city’s vibrant culture. By creating immersive listing content—like videos showcasing nearby music venues or food trucks—sellers can appeal to buyers seeking an authentic Austin experience that new developments may not offer. Partnering with local influencers to promote the home on social media could further boost visibility in a competitive market.

This dataset empowers resale sellers to think strategically. By identifying cities where new construction overshadows resales, sellers can tailor their approach—whether through unique marketing, strategic timing, or creative incentives—to compete effectively. The Austin area’s 2025 housing market, as captured by Team Price Real Estate, provides a roadmap for sellers to navigate and thrive.

FAQ Section

What is the difference between new construction and resale homes in the Austin area?

New construction homes are newly built, often featuring modern designs and warranties, while resale homes are previously owned and may offer established neighborhood charm. In 2025, Austin area data shows new construction often has higher activity indices, like 46.6% in Del Valle, and lower inventory, like 2.27 months, compared to resales at 17.2% and 8.37 months in the same city.

How is the real estate activity index calculated?

The activity index is pending sales divided by the sum of active and pending listings, expressed as a percentage. For example, in Pflugerville’s new construction market, with 53 pending and 65 active listings, the activity index is 53 / (53 + 65) = 44.9%. This shows the proportion of homes under contract.

What does months of inventory mean for Austin area home sellers?

Months of inventory estimates how long it would take to sell all active listings at the current sales rate. In Hutto, new construction’s 2.57 months of inventory versus resales’ 5.45 months suggests new homes sell faster. Sellers can use this to time listings or highlight unique features to compete.

Request Info

Have a question about this article or want to learn more?